The tl;dr about Coast FIRE…

Coast FIRE is when you have enough in your retirement accounts that without any additional contributions, your net worth will grow to support retirement at a traditional retirement age.

I encourage everyone to read up on this very interesting personal finance concept!

Load packages

library(tidyverse)

library(scales)CoastFIRE function

coastfire_calculator <- function(retirement_spend,

withdraw_rate,

growth_rate,

inflation_rate,

retire_age,

current_age){

df <- (retirement_spend) / (withdraw_rate * (1+(growth_rate - inflation_rate))^(retire_age - current_age))

df

}Formula parameters

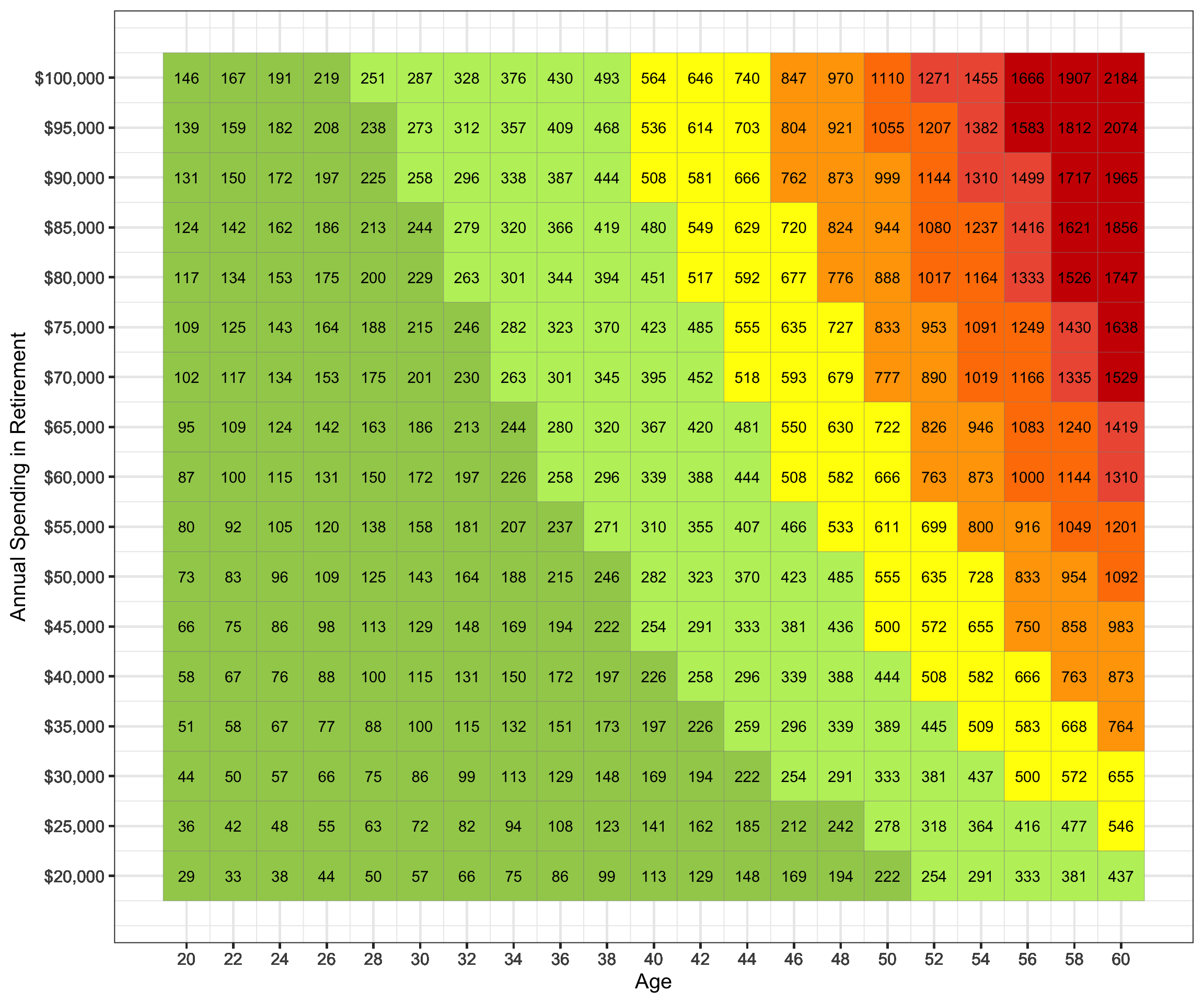

Assumes 3.5% safe withdrawal rate, 8% growth, 3% inflation and retired at 67 years old.

coast_withdraw <- 0.035

coast_growth <- 0.08

coast_inflation <- 0.03

retire_age <- 67Generate dataset

coast_data <- expand.grid(retirement_spending = seq(20000, 100000, 5000),

age = seq(20, 60, 2)) %>%

as_tibble() %>%

mutate(coast_fire = round(coastfire_calculator(retirement_spending,

coast_withdraw,

coast_growth,

coast_inflation,

retire_age, age) / 1000, digits = 0)) Label data

coast_final <- coast_data %>%

mutate(segment = case_when(coast_fire < 250 ~ '0 to $250k',

coast_fire >= 250 & coast_fire < 500 ~ '$250k - $500k',

coast_fire >= 500 & coast_fire < 750 ~ '$500k - $750k',

coast_fire >= 750 & coast_fire < 1000 ~ '$750k - $1M',

coast_fire >= 1000 & coast_fire < 1250 ~ '$1M - $1.25M',

coast_fire >= 1250 & coast_fire < 1500 ~ '$1.25M - $1.5M',

coast_fire >= 1500 ~ '$1.5M+')) %>%

mutate(segment = as.factor(segment))Rearrange factor levels

coast_final$segment <- factor(coast_final$segment,

levels = c("0 to $250k", "$250k - $500k",

"$500k - $750k", "$750k - $1M",

"$1M - $1.25M", "$1.25M - $1.5M",

"$1.5M+"))Visualize data

coast_final %>%

ggplot(aes(age, retirement_spending, fill = segment, label = coast_fire)) +

geom_tile(color = 'gray55') +

geom_text(color = 'black') +

theme_bw() +

scale_fill_manual(values = c("darkolivegreen3", "darkolivegreen2", "yellow1",

"orange1", "darkorange1", "tomato2", "red3")) +

scale_x_continuous(breaks = coast_final$age) +

scale_y_continuous(labels = dollar_format(),

breaks = coast_final$retirement_spending) +

labs(x = "Age", y = "Annual Spending in Retirement", fill = NULL) +

theme_bw(base_size = 15) +

theme(legend.position = 'none')

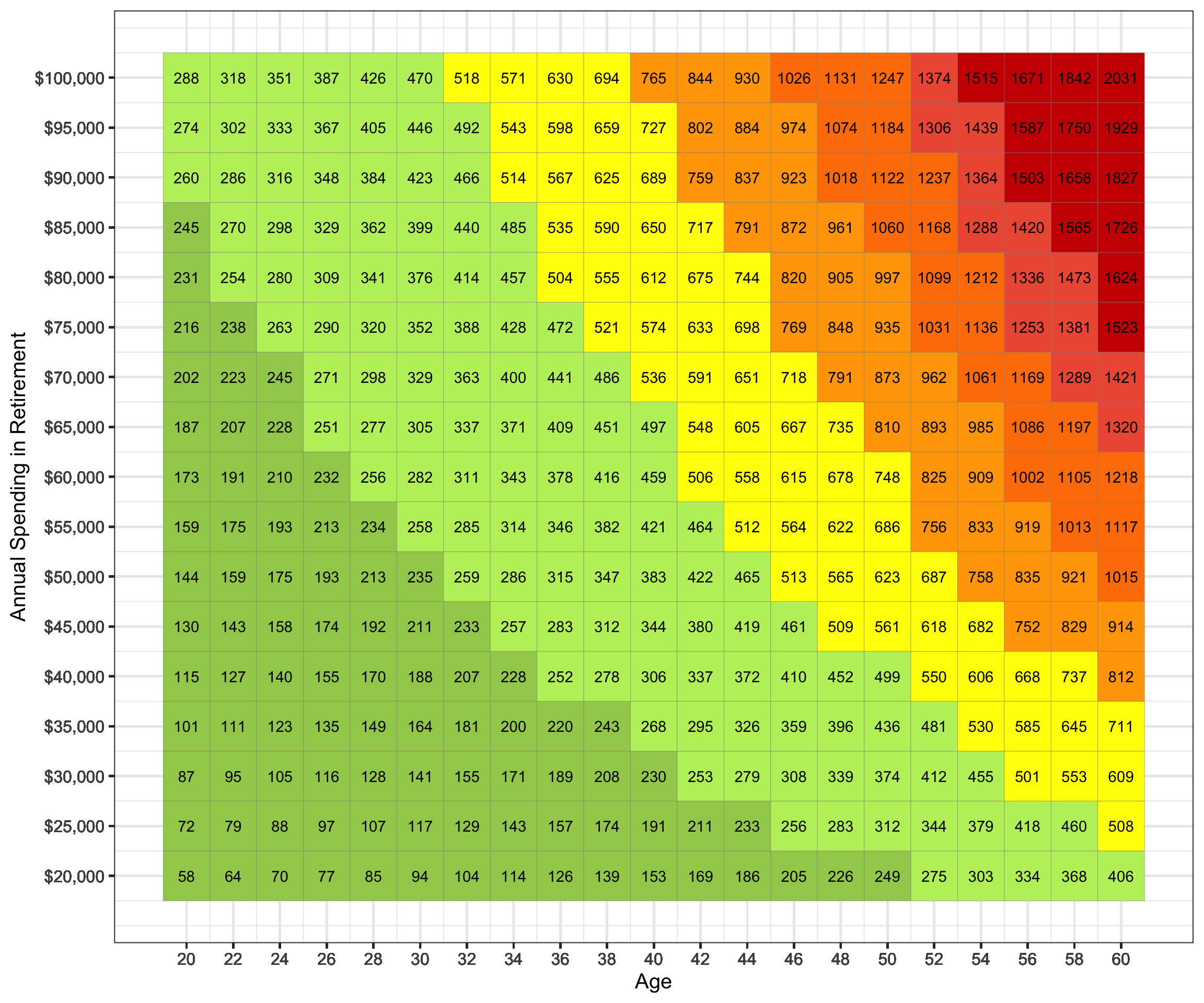

Alternative

The original is a little more on the conservative side so let’s modify slightly with 4% safe withdrawl rate, 10% growth, 3% inflation and retire at 62 instead.